With my limited information, I could surmise that Kiva gives loans to countries that have lithium (Bolivia), for the lithium ion batteries in your laptops and hybrid cars, and coffee (Uganda) because high-end, delicious coffee is market valuable. But there must be more, right?

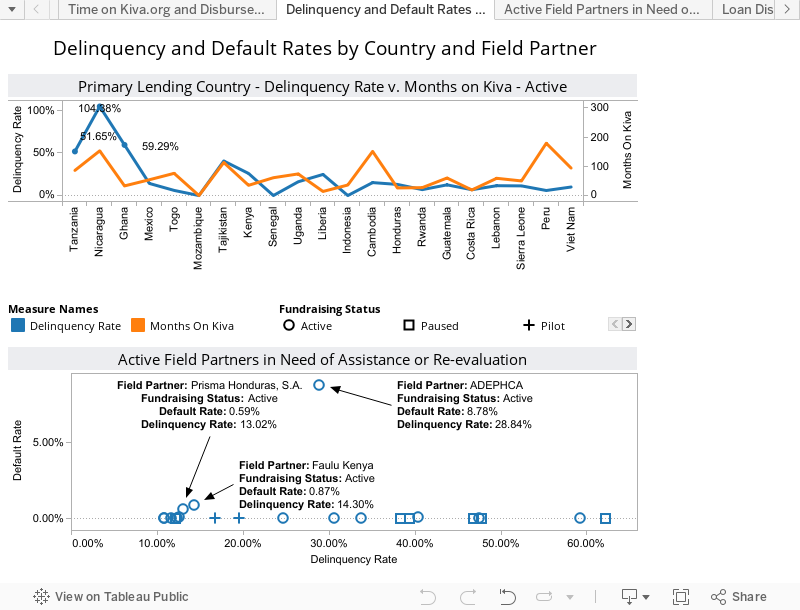

For Bolivia there is. They have a 0.00% delinquency and 0.00% default rate. Stellar! And their economy is growing respectably. In many ways, they've benefitted from the post-Cold War period: even after the West pulled their support in the late 1980s, Bolivia had the second largest reserve of natural gas in South America and now with the growing importance of lithium they have quite a leg to lean on.

But what about Uganda? Uganda is in the Top 5 for delinquency. So why does Kiva loan to them? It could be their vast coffee exports, 56% of GDP. Is that enough? Clearly this warrants more study.

And with all this, what's up with the Dominican Republic? They're in the Top 10 of direct loans from Kiva, but with a considerable default rate. What are they doing that affords them additional funding even with a high default rate?

More importantly, in emerging economies how can we replicate what Bolivia and the others in the Top Tier countries are doing especially with their miniscule default rate?

Stay tuned.